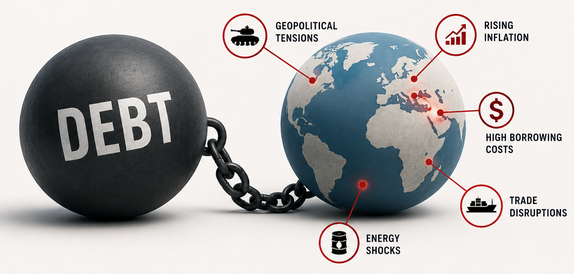

The global economy is entering a dangerous new era defined not only by high debt, but by the convergence of geopolitical conflict, energy insecurity, inflationary pressures, and weakening international cooperation. What once appeared to be isolated economic shocks are increasingly becoming interconnected structural risks capable of destabilizing both advanced and developing economies simultaneously.

The OECD Global Debt Report 2026 revealed that governments and corporations are expected to borrow approximately US$29 trillion from global markets in 2026, representing a 17% increase compared to 2024. Sovereign bond debt in OECD countries has already reached a record US$61 trillion, while global corporate debt has climbed to US$59.5 trillion. At the same time, emerging market and developing economies hold sovereign bond debt worth US$12.1 trillion, with more than half of the low-income countries’ bonds maturing within the next three years. The report reveals a global financial system increasingly dependent on continuous borrowing, refinancing, and investor confidence to sustain economic stability.

Yet the current global environment is far less stable than the one that enabled decades of debt-fueled growth. According to the United Nations World Economic Situation and Prospects 2026 report, global economic growth is projected to decline to 2.7% in 2026, significantly below the pre-pandemic average of 3.2%. Investment remains weak across many regions, while high food, energy, and housing prices continue eroding household incomes and worsening inequality. Although inflation is expected to ease slightly from 3.4% in 2025 to 3.1% in 2026, the world economy is increasingly vulnerable to repeated supply shocks linked to geopolitical tensions, trade fragmentation, and climate disruptions.

One of the clearest signs of this new fragility is the growing relationship between geopolitics and global financial instability. The 2026 IMF/World Bank Spring Meetings highlighted how conflict in the Middle East has intensified energy price volatility, worsening debt burdens across vulnerable economies. The closure of the Strait of Hormuz triggered the largest oil supply shock since World War II, disrupting approximately 20 million barrels of oil per day, equivalent to 20% of global petroleum consumption and nearly one-quarter of global seaborne oil trade. According to the J.P. Morgan Mid-Year Outlook 2026 report, crude oil prices nearly doubled following the escalation, while European liquefied natural gas prices surged by almost 100% within two days. Such developments demonstrate how geopolitical tensions are no longer regional events, as they are global economic risks capable of reshaping inflation, trade flows, financial markets, and debt sustainability simultaneously.

The geopolitical risks extend far beyond energy markets. The global economy has also become dangerously dependent on fragile supply chains concentrated in a small number of strategic regions. The J.P. Morgan report notes that Taiwan produces more than 90% of the world’s advanced semiconductors. Economists estimate that a blockade of Taiwan could reduce global GDP growth by approximately 5%, while the United States economy could contract by 6.7% and China’s economy by 17%. These projections reveal the extent to which economic globalization has created efficiency but simultaneously increased vulnerability. The world economy is now deeply exposed to geopolitical fragmentation, technological competition, and strategic resource dependencies.

At the same time, debt vulnerabilities are intensifying across both advanced and developing economies. Refinancing requirements in OECD countries reached approximately US$13.5 trillion in 2025 and are expected to rise further to US$14 trillion in 2026. The United States and Japan alone account for nearly 80% of these refinancing needs, reflecting the enormous scale of debt accumulation even among the world’s largest economies. Governments are increasingly relying on short-term Treasury bills and shorter-maturity debt instruments to reduce immediate borrowing costs. Treasury bill issuance accounted for approximately 48% of total borrowing in 2025, the highest level since 2009. While this strategy temporarily lowers financing costs, it significantly increases rollover risks because governments must refinance debt more frequently under volatile market conditions.

For developing economies, the situation is even more precarious. Tightening financial conditions, rising interest rates, and geopolitical uncertainty are increasing the risk of sovereign defaults across the Global South. Many low-income countries are now spending more on debt repayments than on development priorities such as healthcare, education, and infrastructure. Some analysts also argue that existing IMF lending approaches emphasizing fiscal consolidation and austerity often weaken long-term development capacity rather than strengthen it. Specifically, research presented by the Boston University Global Development Policy Center suggested that IMF-supported programs have not significantly stimulated productive investment measured through gross fixed capital formation, while austerity-oriented reforms have contributed to rising poverty and environmental degradation.

Africa illustrates many of these global vulnerabilities simultaneously. According to the One Data 2026 report, African countries collectively owed approximately US$707.9 billion in external debt in 2024, with 21 low-income African countries already either in debt distress or at high risk of debt distress. African governments are expected to spend approximately US$84.4 billion on debt servicing in 2024 alone. Meanwhile, 28 African countries now spend more on debt repayments than on healthcare, while 10 spend more on debt servicing than on education. Such trends demonstrate how global debt pressures increasingly translate into social and developmental crises at the national level.

The current global economic trends carry serious implications for businesses, societies, and individuals. Businesses face rising borrowing costs, supply-chain disruptions, energy price volatility, and growing uncertainty caused by geopolitical tensions and slowing global growth. Governments are increasingly diverting resources from healthcare, education, and infrastructure toward debt servicing, worsening inequality and weakening social protection systems. In Africa, many countries now spend more on debt repayments than on healthcare and education combined. For individuals, persistent inflation continues to increase the cost of food, energy, housing, and transport, reducing purchasing power and worsening economic insecurity. Emerging economic pressures threaten long-term economic stability, investment, employment, and sustainable development.

The new global economic fragility is not simply about debt levels or inflation rates in isolation. It is about the dangerous interaction between debt, geopolitics, supply chains, energy security, technological competition, and climate vulnerability.

Join the Discussion

Share your thoughts and engage with the community

Leave a Comment

Comments

No comments yet. Be the first to share your thoughts!